Francophone Africa’s iGaming Landscape: Six Markets, One Opportunity

Emily Thompson

Emily Thompson

There’s a version of the Africa iGaming story that never changes: fast-growing populations, rising smartphone penetration, young demographics, unmet demand. All of that is true. But the picture of Francophone Africa is more specific and more interesting than the continent-wide narrative suggests.

We’ve spent time this year tracking six Francophone African markets: Tunisia, Democratic Republic of Congo, Mali, Côte d’Ivoire, Senegal, and Morocco, and what stands out is how different they are from one another: regulatory approaches, economic profiles, player motivations, and operator landscapes. Grouping them as a single “region” is a shortcut; understanding each on its own terms is where the real opportunity lies.

This report draws on our own market intelligence data collected through April 2026, supplemented by regulatory and industry research to provide the broader market context. For the three deep-dive markets, Tunisia, DRC Congo, and Mali, we have full customer profile survey data from April 2026. For Côte d’Ivoire, Senegal, Cameroon, and Morocco, we cover the market structure, regulatory status, and key growth indicators.

Tunisia: A Betting-Regulated Market with a Shrinking Window

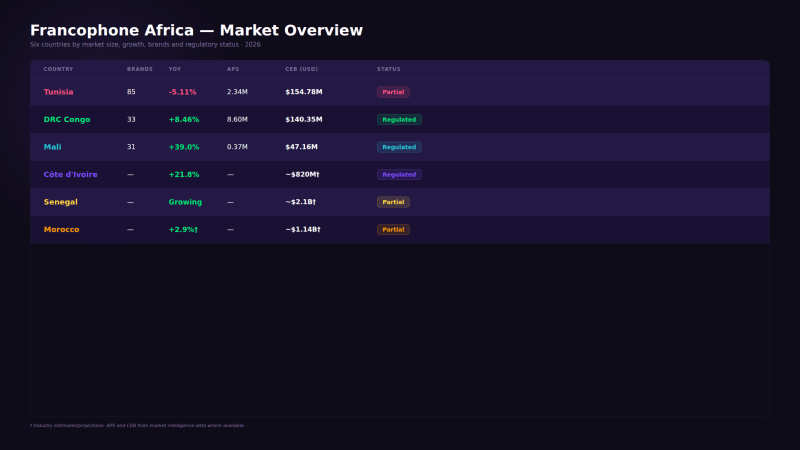

Tunisia sits in an unusual position in the Francophone African context: betting is regulated, but casinos are not. That split regulatory status, combined with the country’s relatively high internet penetration (8.68 million users from a population of 12.05 million, roughly 72%) and a mature digital economy, makes it one of the more complex markets to read in the region.

The market peaked in December 2025 at approximately 4.5 million monthly sessions, then declined steadily through April 2026, during which we recorded 2.34 million APS and $154.78 million in all-time CEB across 85 brands. The year-on-year figure is -5.11%, and the month-on-month is -15.67%. This is a market in contraction, not expansion, and that matters for how operators should be thinking about Tunisia right now.

The brand landscape reflects Tunisia’s dual status. Bet365 leads the all-time table with 310K APS and $21.05M CEB, followed by Forzza ($20.3M) and Icombet ($13.32M). The presence of Bet365 at #1 in a market with 96 total brands is a signal of international operator confidence in the regulated betting framework, even as casino products operate in a legal gray area.

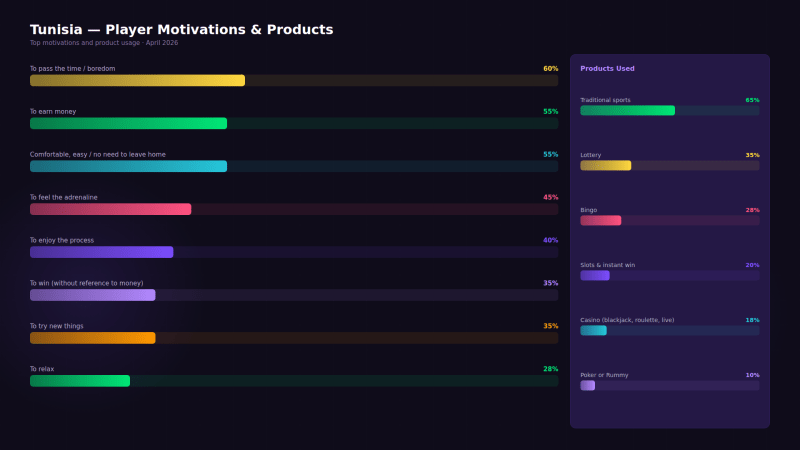

The customer profile in Tunisia is older and more affluent than in most other Francophone African markets. The 25–34 cohort leads at 35%, with the 18–24 group at only 25%, a notably lower youth share than, say, DRC Congo or Mali. Income is concentrated below 10,000 TND annually (65% of respondents in the two lowest brackets), but the high-school-educated majority (35%) and significant university representation (20%) point to a more educated player base than average for the region.

Financial factors drive motivations in Tunisia: earning money (55%), boredom (60%), and comfort/convenience (60%) are the top responses, with comfort/convenience (55%) close behind. Products skew heavily toward traditional sports (65%), then lottery (35%), and slots/instant win (20%). Casino games sit at only 18%, which is consistent with the unregulated casino status limiting product accessibility.

Tunisia is a market in a slow contraction cycle, not a crisis, but not a growth story either. The combination of regulated betting, unregulated casinos, and a shrinking monthly active base means operators here need to compete on retention, not just acquisition.

Democratic Republic of Congo: High Growth, High Risk, Highest At-Risk Rate

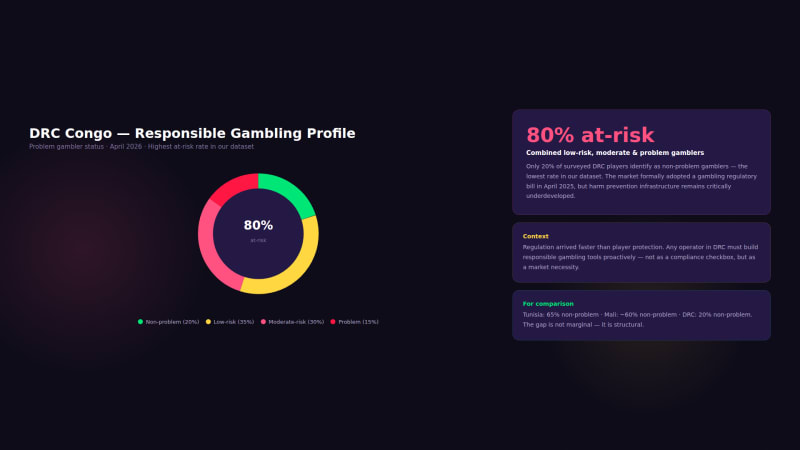

The DRC is the most striking market in our dataset. It has the largest population of the six countries (115.4 million), the highest all-time CEB ($140.35 million), and the most alarming responsible gambling profile of any market we track, 80% of surveyed players fall into at-risk categories.

The market grew sharply through 2025, peaking at approximately 700,000 monthly sessions in December before settling around 460,000 by April 2026. The year-on-year growth rate is +8.46%, with a +1.01% month-on-month rate, making it the only one of our three deep-dive markets showing positive momentum on both measures. Both casino and betting are regulated, which distinguishes DRC from Tunisia and Mali.

Online betting is overwhelmingly dominant: 5.15 million Blask Index vs. 20,000 for online casino, a 250:1 ratio. Betting grew +241.1% year-on-year, making DRC one of the fastest-growing betting markets in sub-Saharan Africa by this measure. betPawa leads with 3.62 million APS and $47.39M CEB (+136.4% YoY), followed by NgeNge ($45.24M) and Winner Bet ($29.68M). The top two brands alone account for approximately 75% of the market’s accumulated power.

The customer profile tells a story of a young, rapidly digitizing population. The 18–24 cohort leads at 35%, with 25–34 at 30%. Income is concentrated in the 1–2 million CDF annual range (30%), which, at current exchange rates, represents a relatively modest disposable income. A high proportion of self-employed players (25%) alongside 40% employed for wages reflects the informal economy’s role in digital adoption.

Responsible gambling data is a number that operators cannot ignore. Only 20% of DRC players identify as non-problem gamblers, the lowest of any market we track. 35% are low-risk, 30% moderate-risk, and 15% are problem gamblers. This is not an artifact of survey design; it reflects a market where gambling infrastructure has grown faster than harm-prevention infrastructure, in a country that only formalized its regulatory framework through a draft bill in April 2025.

An 80% at-risk rate in a regulated market signals that regulation has arrived faster than player protection. Any operator entering DRC that doesn’t build responsible gambling into its core product features is taking on both ethical and long-term reputational risks.

Motivations in DRC lead with financial drivers, earn money (55%), over convenience (45%). Social media dominates discovery at 60%, with mobile app notifications at 45% and online search at 40%. The relatively high TV commercial share (30%) in a market with uneven broadcast infrastructure suggests operators are investing in above-the-line media.

Mali: A Micro-Market with a Concentrated Brand Landscape

Mali is the smallest of our three deep-dive markets by most measures: a population of 21.99 million, 7.48 million internet users, and only 31 active brands. Both casino and betting are regulated under a civil law system derived from the French model. The market is dominated by two operators, Bet223 and Premier Bet, who together account for over 92% of accumulated brand power.

bet223 leads with 2.37 million APS and $21.68 million CEB (+145% YoY), and Premier Bet holds $22.49 million CEB, slightly higher in revenue terms despite lower active sessions. Online betting grew +39.02% year-on-year, making it Mali’s standout category. Online poker is growing (+50.99% YoY) from a small base, and racing and lottery are declining.

The customer profile for Mali reflects the country’s economic reality: only 20% of players are employed for wages, compared to 30% self-employed and 25% unemployed and seeking work. Income is heavily concentrated below 100,000 XOF annually (40%), a very low income threshold. Despite this, the 25–34 age group leads at 35%, and education skews toward high school (40%), with a notable presence at university (15%).

Motivations in Mali are driven by financial factors: earning money (50%) is the clear leader, consistent with an economic profile in which gambling income may represent a meaningful supplementary source. Convenience is lower than in other markets (15%), which is notable given Mali’s lower smartphone penetration (French accounts for only 17.2% of the language distribution, suggesting that a significant portion of the population accesses content primarily in Bambara).

Mali’s iGaming market is real but narrow. Two brands dominate, income levels are low, and the internet-connected population represents about a third of the total. The growth opportunity is real but tightly linked to infrastructure development, mobile penetration, data costs, and mobile money availability.

The Broader Picture: Côte d’Ivoire, Senegal, Cameroon, and Morocco

Beyond our three data-rich markets, the four remaining countries in our coverage area represent a range of market maturities and regulatory trajectories, from Côte d’Ivoire’s state-dominated but rapidly expanding market to Morocco’s two-tier system, where land-based gambling is licensed but online remains in a legal gray zone.

Côte d’Ivoire

Côte d’Ivoire is the largest economy in West Africa and arguably the most commercially dynamic iGaming market in Francophone sub-Saharan Africa. With a population of over 30 million, GDP growth consistently running at 6–7% annually, and smartphone penetration above 50%, the market has the economic foundations to support sustained iGaming expansion.

Industry projections put the overall iGaming market at $820 million in 2026, with sports betting alone estimated at $121 million. LONACI, the state lottery operator, reported 518.36 billion FCFA in revenue in 2023, a 21.84% year-on-year increase. Mobile money accounts for 70–80% of deposits, with Orange Money the dominant payment rail. In October 2025, the ARJH-LONACI-Afitech partnership launched a near-unified national platform for real-time transaction monitoring, making Côte d’Ivoire one of the most technologically advanced regulatory environments in Francophone Africa.

The corporate income tax rate for gambling companies was raised to 30% in 2025, with a 15% withholding tax on winnings. The regulatory direction is toward licensed growth; new licensing for compliant international providers is anticipated as part of ARJH’s 2024–2028 strategic plan.

Senegal

Senegal’s betting market is one of the fastest-growing in the region by headline revenue. LONASE reported CFA 37.2 billion (~$61 million) in revenue in the first half of 2025, and total gambling revenue is projected to reach $2.1 billion by 2026. The first quarter of 2026 saw CFA40.9 billion mobilized, representing a 71% coverage rate of quarterly targets, which the finance minister described as evidence of the sector’s dynamism.

The regulatory picture is more complicated. There are no legislative provisions specifically governing online gambling; it is classified under the 2004 e-commerce law. LONASE holds a monopoly over lotteries and sports betting. Still, Law 17/2025, which introduced a 20% tax on gambling winnings from November 2025, has already triggered market disruption: BetPawa exited the Senegal market in September 2025, citing the adverse conditions the new tax creates for operator economics.

Senegal’s economic momentum is real, 12.1% GDP growth in Q1 2025, driven by hydrocarbon development, but the taxation trajectory and regulatory gray zone for online operators pose material risks to market entry.

Cameroon

Cameroon is one of Central Africa’s most active iGaming markets, with an estimated $290 million in GGR in 2025, of which the online segment accounts for $134 million, growing at approximately 5.2% CAGR through 2029. The country’s bilingual status, French and English, gives it a somewhat distinctive operator landscape relative to purely Francophone markets.

The most significant regulatory development of 2025 was the government’s January centralized payments directive, requiring all online gambling cash flow to pass through INTOUCH Cameroon, a payments aggregator. This real-time transaction monitoring system places Cameroon alongside Côte d’Ivoire as one of the more payment-infrastructure-focused regulatory environments in the region. For operators, compliance with the INTOUCH payments requirement is now a de facto condition for market access.

Morocco

Morocco is the largest and most economically sophisticated of the six markets, with total gambling revenues, including land-based casinos, sports betting, and online, projected at $1.14 billion in 2025, rising to $1.23 billion by 2029. The casino segment alone is expected to generate approximately $700 million in 2025, and sports betting is projected to reach $172 million, growing at a 2.9% CAGR through 2029.

Morocco’s regulatory approach is a two-tier system: land-based gambling is licensed and regulated, while online gambling lacks a domestic licensing framework. The 2025 Finance Bill moved to address the online gap indirectly, by introducing a 30% withholding tax on winnings from foreign online gambling platforms, enforced through Moroccan financial institutions. This creates a taxed-but-unlicensed situation that is familiar to observers of pre-regulation markets elsewhere.

Morocco’s urbanization rate of 64%, relatively high literacy, and GDP per capita of approximately $3,900 make it the most consumer-ready market in this report.

What the Data Tells Us Across All Six Markets

Financial motivation dominates across the region

In all three of our deep-dive markets, “to earn money” ranks among the top motivations. This is markedly different from markets like Ethiopia, where convenience and accessibility lead. The implication for operators is significant: product design, bonus structures, and marketing messaging that lean into the financial opportunity of gambling will resonate more in Francophone Africa than entertainment-first positioning. Jackpot mechanics, cash-out features, and transparent payout rates matter more here than immersive UX or content variety.

Responsible gambling is an underdeveloped priority.

DRC Congo’s 80% at-risk rate is extreme, but it is not an outlier in direction. Across Francophone Africa, formal responsible gambling infrastructure, self-exclusion systems, problem gambling helplines, and mandatory deposit limits are either absent or nascent. Operators entering these markets who implement responsible gambling tools proactively are not just doing the right thing; they are building ahead of where regulation will inevitably go.

Social media is the dominant acquisition channel

Across Tunisia, DRC Congo, and Mali, social media is either the leading or co-leading touchpoint for brand discovery. Facebook, Instagram, TikTok, and Telegram are the primary channels. Online search runs second in Tunisia and Mali, while mobile app notifications are significant in the DRC. TV commercials are more meaningful than in other emerging markets, reflecting the continued relevance of broadcast media in markets where digital content consumption is still developing. Operators who build social-first acquisition strategies will outperform those relying on search alone.

Regulatory convergence is coming

The pattern across all six markets is the same: regulatory frameworks are catching up with market reality. Côte d’Ivoire has a unified transaction monitoring platform. Cameroon mandates centralized payments. Morocco is taxing offshore winnings. Senegal introduced a 20% player tax. DRC formalized a draft gambling bill in April 2025. Tunisia’s split regime is increasingly anomalous. The operators best positioned across Francophone Africa are those building compliance infrastructure now, rather than waiting for each country’s licensing deadline.

Francophone Africa is not one market; it is six distinct regulatory regimes occurring simultaneously. The unifying thread is direction: every country in this report is moving toward more formal oversight, higher taxation, and greater enforcement at the payment layer. The window for easy entry is narrowing.

What We Take Away

Tunisia, DRC Congo, and Mali tell three different stories: a contracting yet sophisticated regulated betting market, an explosive-growth market with a serious responsible gambling problem, and a small but concentrated emerging market dominated by two local operators. Côte d’Ivoire, Senegal, Cameroon, and Morocco add scale, economic weight, and regulatory dynamism to the picture.

The common thread is that all six markets are in motion. Regulatory frameworks are being built or updated, payment infrastructure is being centralized, and player populations are growing faster than harm prevention systems. For operators, the strategic calculus is clear: first-mover advantage in compliance, local payment integration, and responsible gambling infrastructure will define who holds durable market positions in Francophone Africa by 2028.