Inside Brazil’s First Year as a Regulated iGaming Market

Jacob Mitchell

Jacob Mitchell

We have been tracking Latin American iGaming markets for years, and no country has moved faster—or more aggressively—than Brazil. In roughly 18 months, the country transitioned from one of the world’s largest unregulated online betting gray markets to a fully licensed federal regime. Moreover, the numbers from year one are staggering.

When we first started covering Brazilian operators, the landscape was fragmented. Dozens of international brands operated in a legal gray zone, players had few formal protections, and nobody could say with confidence how big the market actually was. That changed on January 1, 2025, when federal authorization became the gatekeeper for nationwide online betting and gaming.

Now we have official data from Brazil’s Secretariat of Prizes and Betting (SPA), and the picture it paints is extraordinary: BRL 36.96 billion in gross gaming revenue in 2025, 25.25 million unique bettors, and more than 100 million brand accounts across licensed platforms. This is no longer an emerging market. It is the largest regulated online gambling market in Latin America, and its trajectory matters for every operator and affiliate working in the region—including markets like Argentina, where the regulatory conversation is heading in a similar direction.

This post draws on official SPA reports, Central Bank data, industry forecasts, and our own experience ranking operators across Brazil and Argentina. We are going to walk through what happened, why it matters, and what comes next.

Brazil iGaming Market Timeline — Key Regulatory Milestones from 2018 to 2026, showing the staged path from legalization to full operational regulation

The Regulation Was Not a Single Event—It Was a Rolling Build

One thing we have noticed when talking to operators and industry contacts is a common misconception: that Brazil “legalized” betting in 2023 or 202,4 and that was that. The reality is much more layered.

The statutory foundation was laid back in December 2018 when Law No. 13,756 legalized fixed-odds betting as a lottery modality. Nevertheless, the market then grew for years without a complete operational rulebook. The decisive shift came with Law No. 14,790 in December 2023, which formalized taxation, advertising restrictions, sanctions, responsible-gaming obligations, and the inclusion of online games within the fixed-odds framework.

What followed in 2024 was an extraordinary regulatory sprint. The SPA issued ordinance after ordinance—on payment transactions (Portaria 615), technical and security requirements (Portaria 722), authorization rules (Portaria 827), AML/CFT obligations (Portaria 1,143), and responsible-gaming rules (Portaria 1,231). By September 2024, the regulator had limited the transitional market to applicants already in process.

Brazil’s regulation is cumulative, not static. Operators have had to adapt not just to licensing but also to a rolling program of payments, AML, self-exclusion, health, and enforcement measures that continues through 2026.

Moreover, it has not stopped. In late 2025, the SPA strengthened auto-limits and launched a centralized self-exclusion platform. In March 2026, Law No. 15,358 introduced payment data interoperability and enhanced due diligence requirements. For operators used to lighter-touch jurisdictions, the pace and depth of Brazil’s regulatory accumulation have been genuinely demanding.

The Numbers: What Year One Actually Looked Like

We spend a lot of time parsing market data from different sources, and what makes Brazil interesting is that we now have official regulator numbers to work with rather than relying solely on industry estimates.

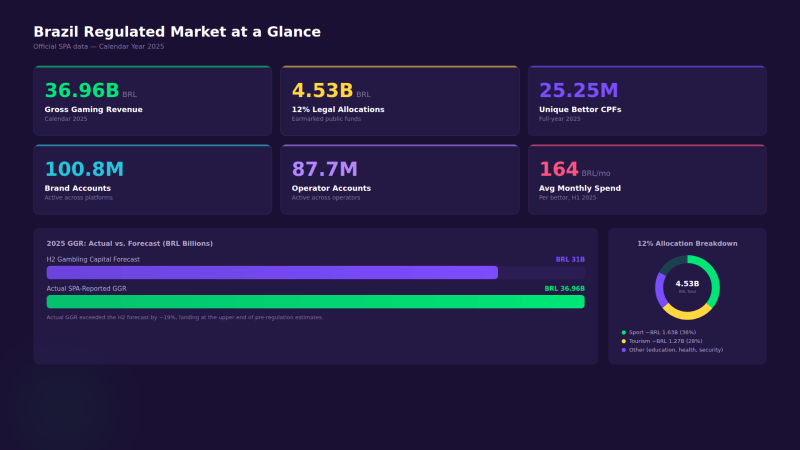

The SPA’s year-end 2025 report confirmed:

- BRL 36.96 billion in gross gaming revenue for calendar year 2025

- BRL 4.53 billion in 12% legal allocations earmarked for public purposes

- 25.25 million unique bettor tax IDs (CPFs)

- 100.8 million brand accounts and 87.7 million operator accounts

Average effective spend of approximately BRL 983 per bettor in the first half, or about BRL 164 per month.

Brazil Regulated Market at a Glance — GGR, unique bettors, brand accounts, and allocation totals for 2025 (infographic-style summary)

For context, the widely cited H2 Gambling Capital forecast had projected around BRL 31 billion in GGR for 2025. The actual result landed well above that. It also broadly matched the upper end of what the Central Bank’s Pix-based analysis had implied about pre-regulation market size—suggesting that legalization did not create the market so much as it formalized a market that was already massive.

The multi-homing numbers jumped out at us immediately. With 25.25 million unique bettors corresponding to roughly 87.7 million operator accounts, that implies about 3.5 active operator accounts per bettor over the year. We see this reflected in our own data—Brazilian players are comparison-shopping aggressively, and loyalty is hard to earn.

Multi-Homing Behavior — Ratio of unique bettors to active operator accounts and brand accounts, illustrating the extreme account fragmentation

How Operators Are Entering: Three Playbooks We are Watching

From our vantage point, ranking and reviewing operators across Brazil’s regulated market, we have identified three distinct entry strategies playing out in the post-regulation landscape.

Direct Licensed Entry

The most straightforward path. International brands like Bet365, Betfair, Sportingbet, Novibet, Pinnacle, and Betano have established or used Brazilian legal entities to apply directly for federal authorization. These operators localize their domains under the mandatory “.bet.br” extension and build out the full compliance stack locally. It’s capital-intensive—a BRL 30 million authorization fee for five years, covering up to three brands—but it’s the clearest path for well-resourced global operators.

Partnership-Led Distribution

The MGM Resorts and Grupo Globo venture to launch BetMGM Brazil is the headline example here. Pairing a global operator brand with Brazil’s dominant media group gives the venture built-in audience reach and cultural credibility that money alone cannot buy quickly. We expect to see more of these structures as operators recognize that local distribution matters as much as product quality in a market this competitive.

M&A-Led Consolidation

Flutter’s acquisition of a controlling stake in NSX, owner of Betnacional, is the most significant deal we have tracked. This was not just a brand acquisition—it was a speed-to-scale play that brought local operating capability, existing player relationships, and regulatory experience under one roof. In a market where compliance depth and local knowledge are structural advantages, buying a credible local brand can be worth more than building from scratch.

The regulatory economics in Brazil favor scale, depth of compliance, and strong local distribution over pure brand awareness. A market with BRL 30 million authorizations and massive multi-homing does not reward timid, undercapitalized entrants.

Operator Entry Strategy Map — Visual comparison of direct licensing vs. partnership vs. M&A approaches, with key examples and trade-offs

Payments, KYC, and AML: The Compliance Stack Is the Product

If there is one thing we would tell any operator or affiliate partner considering Brazil, it is this: compliance is not a cost center in this market. It is the product.

Brazil’s payments architecture is tightly coupled to domestic digital-payments rails. The law requires prize payments to be made only into bank or payment accounts owned by the bettor, maintained at institutions headquartered in Brazil and authorized by the Central Bank. Operators have a 120-minute maximum payout window after a sporting event or online game session ends. In practice, this means the Pix-based instant payment culture that Brazilian consumers expect is not just a preference; it is a regulatory requirement.

KYC has become progressively more intrusive. The SPA’s rules allow facial recognition in key account-management steps and even permit operators to request proof of income. Law No. 15,358 of March 2026 further extended the payment perimeter by requiring financial institutions to integrate with interoperable fraud information-sharing systems and adopt enhanced due diligence to prevent transactions with unauthorized operators.

AML obligations are built on Brazil’s existing anti-money-laundering law (Law 9,613/1998) and aligned with FATF principles. Suspicious transactions must be reported to Coaf, and the SPA has held operator guidance sessions on reporting standards.

Brazil’s regulator is trying to solve illegal-market leakage through the payments layer as much as through ISP blocking. That makes the payments stack a frontline competitive tool rather than a back-office function.

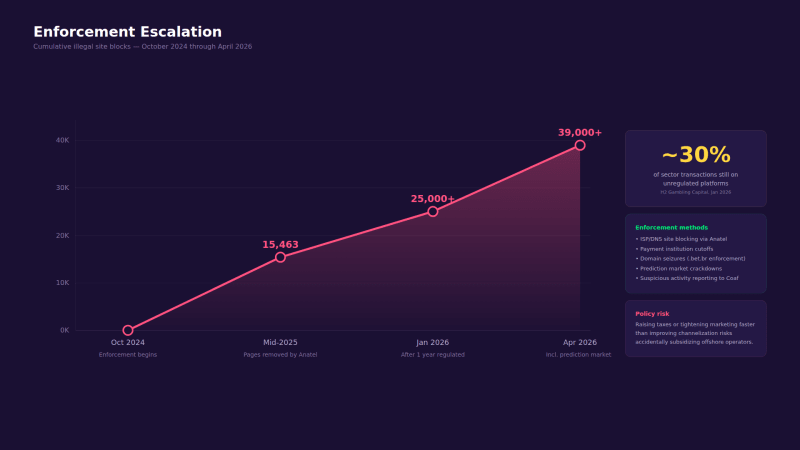

The Channelization Challenge: 39,000 Sites Blocked and Counting

We have watched enforcement ramp up dramatically since the regulation took effect. The numbers tell the story:

- By mid-2025, more than 15,000 illegal pages had been removed by Anatel since October 2024

- After one full year of regulated operation, more than 25,000 illegal sites had been blocked

- By April 2026, enforcement against illegal bets and adjacent “prediction markets” had led to blocks of more than 39,000 sites

The government has also forced payment institutions to refuse or terminate service for illegal operators. That is a meaningful escalation—it attacks the financial infrastructure of unlicensed platforms, not just their web presence.

However, the illegal market problem remains material. H2-linked estimates from early 2026 put roughly 30% of sector financial transactions on unregulated platforms. That is far below some more alarmist claims, but it is still big enough to distort competition, tax collection, safer-gambling coverage, and brand economics.

Enforcement Escalation — Cumulative illegal site blocks from October 2024 through April 2026, with key enforcement milestones annotated

The policy implication is one we discuss regularly in our coverage: if Brazil raises taxes or tightens marketing faster than it improves channelization, it can accidentally subsidize the offshore market. This tension is not theoretical—it is actively shaping regulatory decisions.

The Social Ledger: Real Concerns, Real Responses, Real Gaps

We do not shy away from the harder questions, and the social impact data from Brazil demands honest engagement.

The Central Bank’s 2024 study estimated about 24 million individuals sent money to betting and gambling companies via Pix. More striking, 5 million Bolsa Família beneficiary households transferred BRL 3 billion to betting firms in August 2024 alone, with a median spending of BRL 100. Around 17% of registered Bolsa Família beneficiaries bet during the period under analysis.

Those numbers are not the prevalence of gambling disorder—they are participation and vulnerability indicators. Nevertheless, they are serious enough to explain why Brazil’s health and finance authorities escalated the issue into a multi-ministry problem.

The health system response is underway, but still catching up. Brazil’s TCU (federal audit court) found weak coordination, limited indicators, and low readiness—55.2% of SUS health professionals reported not feeling prepared to treat betting addiction. In response, the Health Ministry issued guidance in 2025, launched a national care guide in January 2026, and started free tele-mental-health services through SUS in March 2026, initially serving 600 patients per month.

The centralized self-exclusion platform, which went live in December 2025, received more than 217,000 self-block requests by January 2026. That is a meaningful signal that the tool is reaching people who need it, though the scale of the market—25 million bettors—puts even that number in perspective.

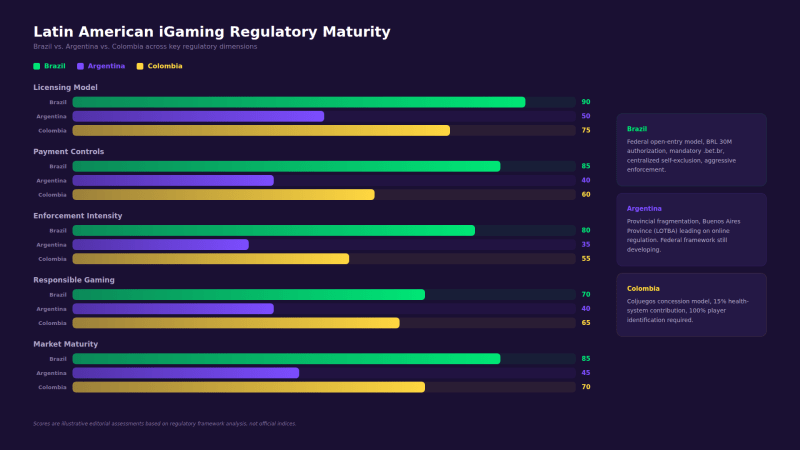

Why This Matters for Argentina and the Wider Latin American Market

We cover both Brazil and Argentina closely, and one thing is increasingly clear: Brazil’s regulatory choices are setting the benchmark for the entire region.

Argentina’s iGaming landscape remains fragmented across provincial jurisdictions, with Buenos Aires Province (LOTBA) leading the way in online regulation. However, the conversation among Argentine regulators, operators, and industry participants is already being shaped by what Brazil has done—both the ambitions and the cautionary tales.

Several of Brazil’s regulatory innovations are directly relevant to Argentina’s trajectory: centralized self-exclusion systems, mandatory domestic payment processing, aggressive enforcement against unlicensed operators, and earmarked social allocations from gaming revenue. The question for Argentina is not whether to regulate more comprehensively—it is how fast to move and which elements of Brazil’s model to adopt or adapt.

For operators active in both markets—and we rank several that are—the lesson is to invest in compliance infrastructure that scales across Latin American jurisdictions rather than building one-off solutions for each country. The operators who get Brazil right will have a significant head start when Argentina and other regional markets tighten their frameworks.

Latin American iGaming Regulatory Maturity Comparison — Brazil vs. Argentina vs. Colombia on key regulatory dimensions (licensing model, payment controls, enforcement intensity, responsible gaming)

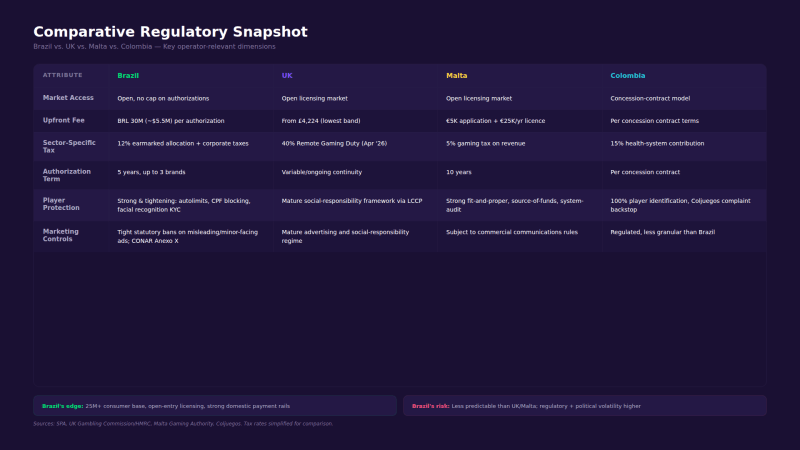

Brazil Compared: How It Stacks Up Against the UK, Malta, and Colombia

Context matters, so here is how Brazil’s approach compares to three reference jurisdictions on a practical operator basis:

- Against the UK: Britain emphasizes mature licensing plus high product-specific gambling duties (remote gaming duty rising to 40% from April 2026). Brazil’s sector-specific take is lower, at a 12% earmarked allocation, but ordinary corporate taxes sit on top, making the full effective burden harder to calculate. The UK has a more established responsible-gambling framework; Brazil’s is newer but evolving rapidly.

- Against Malta: Malta’s 5% gaming tax on revenue is lower, and its EU/EEA-oriented licensing model is more internationally streamlined. However, Malta’s market is the operator base, not the consumer market. Brazil offers a domestic consumer base of 25 million+ active bettors—a fundamentally different value proposition.

- Against Colombia: Colombia’s Coljuegos concession model is the closest Latin American comparator. Colombia requires a 15% health-system contribution from operators’ monthly gain, which is directionally similar to Brazil’s earmarked allocations. Nevertheless, Brazil’s open-entry model (no cap on authorizations) differs from Colombia’s concession-contract approach, and Brazil’s market is dramatically larger.

Comparative Regulatory Snapshot — Brazil vs. UK vs. Malta vs. Colombia across key operator-relevant dimensions (market access, fees, tax burden, player protection, marketing controls)

Three Scenarios for What Comes Next

- Base case: Continued growth under a stricter regime. Brazil keeps nationwide online betting legal, raises enforcement intensity, pushes more traffic to “.bet.br,” deepens self-exclusion and payment screening, and possibly edges tax rates upward without destroying channelization. Quality operators consolidate share while weaker firms exit. This is the scenario we consider most likely and the one we are planning around.

- Downside: Regulatory overcorrection. If Brasília sharply raises the sector-specific take, broadens advertising bans, or pursues politically driven restrictions without corresponding channelization improvements, the market could bifurcate—a heavily burdened onshore core alongside a material offshore fringe. President Lula’s April 2026 comments supporting a potential national ban on online platforms, while likely requiring difficult legislative action, put this branch firmly on the strategy map.

- Upside: Institutional maturation. If the SPA continues to publish credible market data, payment institutions improve interdiction of illegal operators, and health policy coordination strengthens, Brazil could become the largest sustainable, regulated online gambling market in Latin America with a defensible social license. The 2025 market reporting and 2026 agenda already point in this direction.

Brazil is no longer a ‘light-touch, sponsor-the-shirt-and-scale’ opportunity. It is becoming a fully regulated, full-stack market in which payments, data traceability, responsible gaming, advertising discipline, and political resilience matter as much as product.

What We are Telling Operators and Partners

Based on everything we have tracked—and based on our own experience ranking, reviewing, and steering players toward responsible, licensed operators across Brazil—here is our practical takeaway for the industry:

- Build local payments and KYC as core product infrastructure, not a compliance afterthought. Brazil’s Pix-centric payment culture and the regulator’s insistence on domestic financial rails mean that payment speed and reliability are competitive differentiators, not checkboxes.

- Optimize for channelization-friendly trust signals. The “.bet.br” domain, fast payouts, clean advertising, visible dispute-resolution routes through Consumidor.gov.br—these are the signals that help players choose licensed over unlicensed. Every operator should be making it easy for players to verify legitimacy.

- Assume multi-homing is structural. With 3.5+ operator accounts per bettor, retention economics matter more than acquisition fireworks. Bonusing discipline, personalization, and consistent player experience are what keep bettors from spreading their activity even further.

- Model the political downside explicitly. Brazil now deserves a policy-risk discount rate. The regulatory environment is favorable today, but the political conversation has shifted—operators who do not scenario-plan for tax increases or marketing restrictions are taking on risks they have not priced in.

- Watch Argentina. The regulatory frameworks being tested in Brazil—centralized self-exclusion, mandatory domestic payments, earmarked social allocations—are setting a template. Operators building scalable compliance infrastructure across Latin America, rather than country-by-country patches, will have a meaningful advantage as Argentina’s market continues to formalize.

The Bottom Line

Brazil’s first year of regulated iGaming confirmed what many of us in the industry suspected: this was already one of the world’s biggest online gambling markets, and formalization has only accelerated its growth. BRL 36.96 billion in GGR, 25 million bettors, and a regulatory framework that is still actively tightening—these are not numbers that can be hand-waved away.

However, growth is not the whole story. The channelization challenge remains real, the social-impact questions are serious, and the political environment has become less predictable. The operators who will thrive are those who treat Brazil as what it is: a full-stack, regulated market that demands depth of compliance, local expertise, and the kind of player trust that takes years to build and seconds to lose.

We are committed to tracking this market closely—both in Brazil and across the broader Latin American landscape, including Argentina. The data is clear, the market is real, and the regulatory framework—for all its complexity—is a net positive for players and for the long-term health of the industry.

We will continue publishing updated operator rankings, market analysis, and regulatory tracking throughout 2026. If you are operating in or entering the Brazilian market, the time to invest in compliance, local capability, and player trust is now—not next quarter.